7 Home Buying Myths in 2026 That Are Holding You Back — And the Truth You Need to Hear

Introduction

Did you know that nearly 70% of first-time home buyers say they waited longer than necessary to buy — often because of something they believed that simply wasn’t true? Home buying myths are everywhere, and they can be surprisingly costly. They can delay your purchase by years, drain your savings chasing the “perfect” scenario, or convince you that homeownership is out of reach when it’s closer than you think.

At Sievers Real Estate, we talk to buyers every day who are surprised to learn the truth behind these common misconceptions. Whether you’re a first-time buyer or returning to the market, busting these home buying myths could be the first step toward finding your next home sooner than you imagined.

Let’s set the record straight.

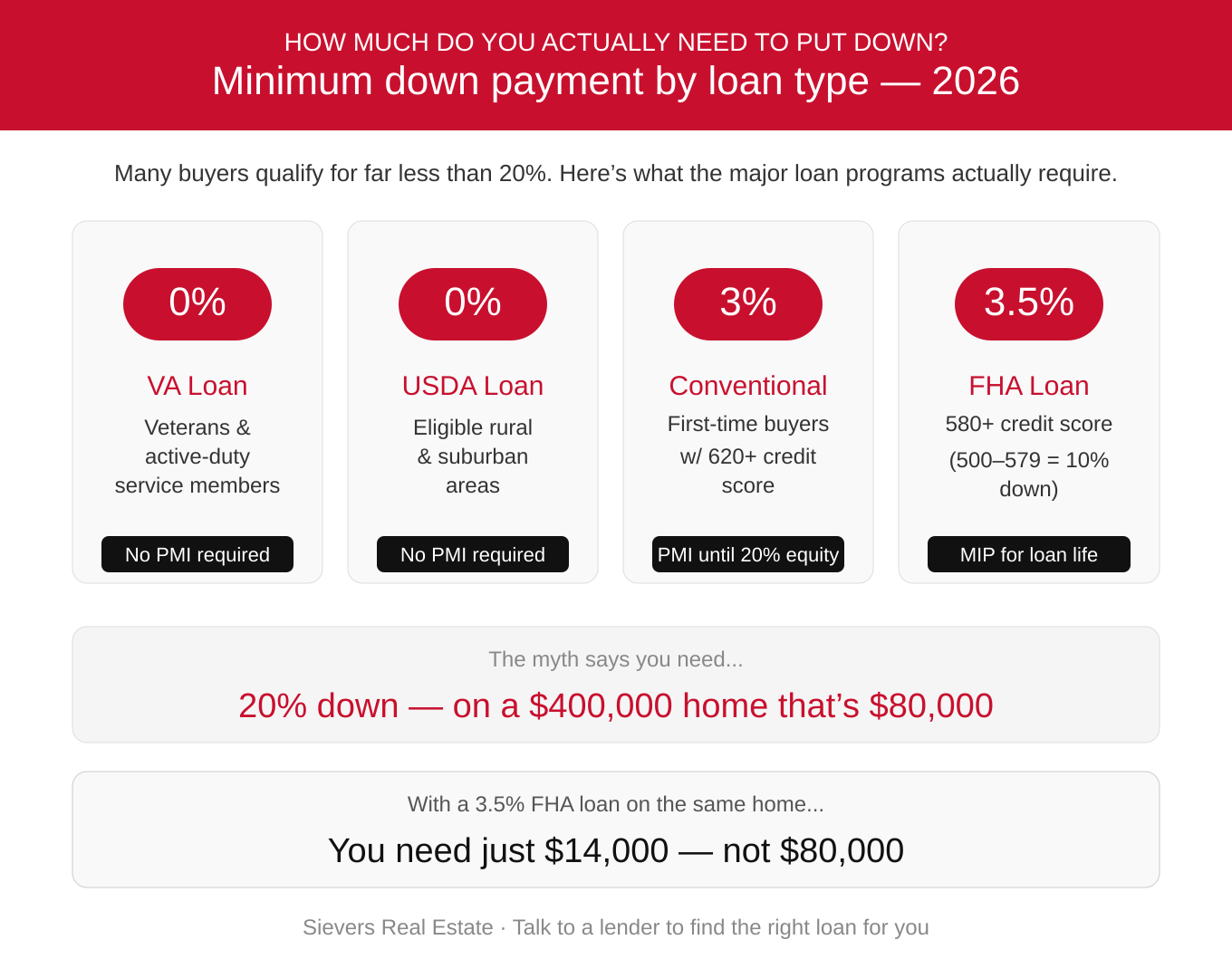

Myth #1: You Need a 20% Down Payment to Buy a Home

The Truth: Many Buyers Put Down Far Less — and Still Get Great Loans

This is arguably the most persistent home buying myth, and it stops more buyers in their tracks than any other. The idea that you must save 20% before even thinking about buying a home is simply outdated.

Here’s what down payment options actually look like today:

- FHA Loans: As low as 3.5% down with a qualifying credit score of 580+

- Conventional Loans: Some programs allow as little as 3% down for first-time buyers

- VA Loans: 0% down for eligible veterans and active-duty service members

- USDA Loans: 0% down for buyers purchasing in eligible rural areas

Where did the 20% myth come from? Putting down 20% allows buyers to avoid Private Mortgage Insurance (PMI) — an added monthly fee that protects the lender. While avoiding PMI is a nice goal, it’s absolutely not a requirement to purchase a home. Many buyers choose a lower down payment now, build equity, and refinance later.

|

💡 Quick Tip Talk to a lender before you assume you’re not ready. You may qualify for a loan program that requires far less than you think. |

Myth #2: You Need Perfect Credit to Get a Mortgage

The Truth: Many Loan Programs Accept Credit Scores in the 580–640 Range

Another of the most common home buying myths is that only buyers with pristine credit scores can qualify for a mortgage. While a higher credit score certainly earns better interest rates, it is not the only path to homeownership.

Here’s a general breakdown of credit score thresholds by loan type:

- FHA Loans: Minimum score of 580 (or 500 with 10% down)

- VA Loans: No official minimum, though most lenders look for 620+

- Conventional Loans: Typically 620+ preferred

- USDA Loans: Generally 640+ recommended

If your credit score isn’t where you’d like it to be, don’t give up. Simple steps like paying down credit card balances, avoiding new debt, and correcting errors on your credit report can meaningfully raise your score in 3–6 months.

|

💡 Quick Tip A good real estate broker can connect you with lenders who specialize in helping buyers with non-traditional credit profiles. The Sievers Real Estate team is happy to make those introductions. |

Myth #3: Renting Is Always Cheaper Than Buying

The Truth: In Many Markets, a Mortgage Payment Is Comparable to — or Less Than — Rent

With rents rising steadily in many cities, the assumption that renting is the more affordable option deserves a closer look. When you rent, you’re building your landlord’s equity, not your own.

When you buy, every mortgage payment works in your favor through:

- Equity building: Your home’s value grows over time (historically, U.S. home values appreciate around 3–5% annually)

- Tax advantages: Mortgage interest and property taxes may be deductible

- Payment stability: A fixed-rate mortgage keeps your payment consistent, unlike rent that can increase every year

- Wealth building: Homeownership remains one of the most reliable ways to build long-term wealth

Of course, buying isn’t right for everyone in every situation. But the blanket assumption that renting is always smarter financially is one of the most common home buying myths we encounter.

Myth #4: You Should Wait for the “Perfect” Market

The Truth: Trying to Time the Market Is a Risky Game

Many buyers sit on the sidelines waiting for home prices to drop or interest rates to fall. While it’s smart to be strategic, trying to “time the market” is one of the most costly home buying myths buyers can act on.

Here’s why:

- Real estate markets are unpredictable. Experts routinely miss the mark on where rates and prices are headed.

- Every month you wait, you’re paying rent instead of building equity.

- When rates do drop, buyer competition spikes — often driving prices back up.

- The best time to buy is typically when you’re financially ready and find a home that fits your needs.

As the National Association of Realtors consistently notes, buyers who wait for the “perfect” time often pay more in the long run than those who bought during imperfect conditions.

|

💡 Quick Tip Focus on what you can control: your credit score, your savings, and your readiness. The Sievers Real Estate team can help you evaluate whether now is a good time for your personal situation. |

Myth #5: You Don’t Need a Real Estate Broker as a Buyer

The Truth: Buyer’s Brokers Are Usually Free to the Buyer — and Invaluable

Some buyers assume they can navigate the home buying process alone, especially with online listings readily available. But this is one of the home buying myths that can genuinely cost you money and stress.

A buyer’s broker brings:

- Market expertise: They know what homes are actually worth and how to negotiate effectively

- Access to listings: Including off-market and pre-market opportunities

- Contract knowledge: Protecting your interests through complex legal documents

- Negotiation skills: Skilled brokers routinely save buyers thousands of dollars

- Local connections: From inspectors to lenders to title companies

And here’s the part many buyers don’t realize: in most transactions, the seller pays the buyer’s broker commission. Working with a skilled real estate broker typically costs buyers nothing out of pocket.

Myth #6: The List Price Is the Final Price

The Truth: Nearly Everything in Real Estate Is Negotiable

Many first-time buyers assume the asking price is set in stone. This is one of the home buying myths that leaves real money on the table.

In most transactions, there is room to negotiate:

- Purchase price: Especially in a buyer’s market or if a home has been sitting on the market

- Closing costs: Sellers can be asked to cover some or all closing costs

- Repairs: After a home inspection, buyers can request repairs or price reductions

- Contingencies: Inspection, financing, and appraisal contingencies all protect the buyer

- Move-in dates and personal property: Often negotiable as part of the deal

An experienced broker knows what’s reasonable to ask for and how to make an offer that gets accepted without leaving value behind.

Myth #7: Pre-Qualification and Pre-Approval Are the Same Thing

The Truth: Pre-Approval Carries Far More Weight in Today’s Market

These two terms sound similar but are very different — and confusing them is one of the home buying myths that can cost buyers their dream home.

- Pre-Qualification: A rough estimate based on self-reported financial information. Quick, but not verified. Sellers and listing brokers don’t put much weight on this.

- Pre-Approval: A lender has actually reviewed your income, assets, credit, and employment. This is a conditional commitment to lend you money up to a specific amount. Sellers take pre-approved buyers much more seriously.

In competitive markets, a pre-approval letter is often the difference between having your offer accepted and losing the home to another buyer. Get pre-approved before you start seriously shopping.

|

💡 Quick Tip Getting pre-approved takes as little as a few days and costs nothing. Contact Sievers Real Estate and we’ll connect you with a trusted local lender. |

Bonus: A Few More Myths Worth Busting

- "I have to find the home before talking to a lender." — Start with a lender. Knowing your budget makes your search faster and more focused.

- "New construction homes don’t require inspections." — Always get an inspection, regardless of age or condition.

- "I should max out my pre-approval budget." — Just because you’re approved for a certain amount doesn’t mean you should spend it all. Consider total monthly costs, including taxes, insurance, HOA fees, and maintenance.

- "A bigger home is always a better investment." — Location, condition, and market demand matter far more than square footage.

The Bottom Line

Home buying myths are more than just misconceptions — they can delay your journey to homeownership by months or even years. The good news? None of the myths above have to hold you back any longer.

Whether you’re wondering if you qualify for a low down payment mortgage, trying to figure out if your credit score is good enough, or unsure whether now is the right time to buy, the first-time home buyer tips that matter most always start with getting accurate, personalized guidance.

At Sievers Real Estate, we’re here to give you the straight answers you need — no jargon, no pressure, no myths.

Ready to Start Your Home Search?

Contact the Sievers Real Estate team today for a free consultation. We’ll walk you through your options, connect you with a trusted lender for pre-approval, and help you find a home that fits your life and your budget.

📞 Schedule a Free Consultation | 🏠 View Current Listings | ✉️ Subscribe to Our Newsletter

Recent Posts

GET MORE INFORMATION